BY GEORGE SOUTO

Mortgage and Lending with George Souto

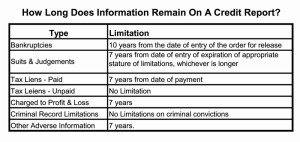

Often I pull credit reports which the Borrower claims a debt is being reported incorrectly. Fortunately we have a process to assist them for free through our Credit Report Company, but for those who do not have that option, they need to know the steps to correct the errors on their own.

Finding a debt being reported in error is not the kind of SURPRISE anyone wants to see when they are reviewing their Credit Report. So What Can Be Done To Correct Errors On A Credit Report?

As I mentioned above, when I review a Credit Report with a Borrowers, and one of their Creditors has incorrectly reported a:

Late Payment

Collection

Judgment

I first instruct the Borrower to contact the Credit Reporting Company I use, and they assist the Borrower in making the necessary disputes to correct how the item(s) is being reported on their Credit Report for free. Most Creditors report monthly to all three Credit Bureaus Equifax, Experian, or TransUnion. Therefore, the dispute needs to be submitted to all three in order to correct the mistake and adjust the Credit Scores. I instruct the Borrower to send proof the item(s) were paid to the Credit Reporting Company I use, and a dispute is filed on behalf of the Borrower with all three Credit Bureaus.

However, those who are not applying for a Mortgage, and therefore, do not have access to this free service, they need to do the following to correct the items reported incorrectly on their Credit Report.

They will need to write a letter of dispute to each of the three Credit Bureaus Equifax, Experian, or TransUnion along with proof the items they are disputing are being reported incorrectly. The letter needs to include the Trade Line, Account Number(s), and reason why they believe it is reporting incorrectly.

Under the Fair Credit Reporting Act, each Credit Bureaus must contact the Creditor or person the dispute is being filled against within 5 days of the receipt of the request. The Creditor or person the dispute is filled against then has to give a written reply back to the Credit Bureaus within 30 days of the date the dispute was filled.

The Credit Bureaus then have 5 days from receipt of the creditor’s or person’s written reply, to provide a written report with their findings. They will also need to provide a copy of a revised Credit Report if changes were made.

So what happens if the procedure above is not followed? There are 3 possible scenarios:

No response from the Creditor or person the dispute is filled against. If that happens the data is removed.

The Creditor or person that the dispute is filled against shows proof they are correct. If that is the case the data remains.

The Creditor or person the dispute was filled against acknowledges they were wrong or partially wrong, and they correct the item(s) they are reporting incorrectly.

In each of the above scenarios the person who submits the dispute must be notified by the Credit Bureaus of the results, but there is one little twist to the first scenario. If the Creditor or person who the dispute was filled against does not respond within the required time period, and the correction is made, the error can still show up later if the creditor at a later date decides to report the item again. So if the correction is made because the Creditor or person the dispute was filled against did not respond, the person who submitted the dispute must continue to monitor their Credit Report, because the error could show up again at a later date.

Everyone is entitled to one free Credit Report per year from each of the Credit Bureaus. It is wise to take advantage of this every year, so if a Creditor is reporting something incorrectly, or if fraud is going on, it can be addressed quickly.

Hopefully those reading this blog will never have anything reported incorrectly on their credit report. But if there are errors just follow the steps above for What Can Be Done To Correct Errors On A Credit Report, and the errors should be corrected within 30 days.